Income tax is a fundamental aspect of a country’s fiscal policy, and understanding the income tax slabs for each financial year is crucial for taxpayers to effectively plan their finances. In this article, we will delve into the income tax slabs for FY 2023-24 (AY 2024-25) under the new tax regime, providing detailed insights and calculations.

Income Tax Slabs for FY 2023-24 (AY 2024-25)

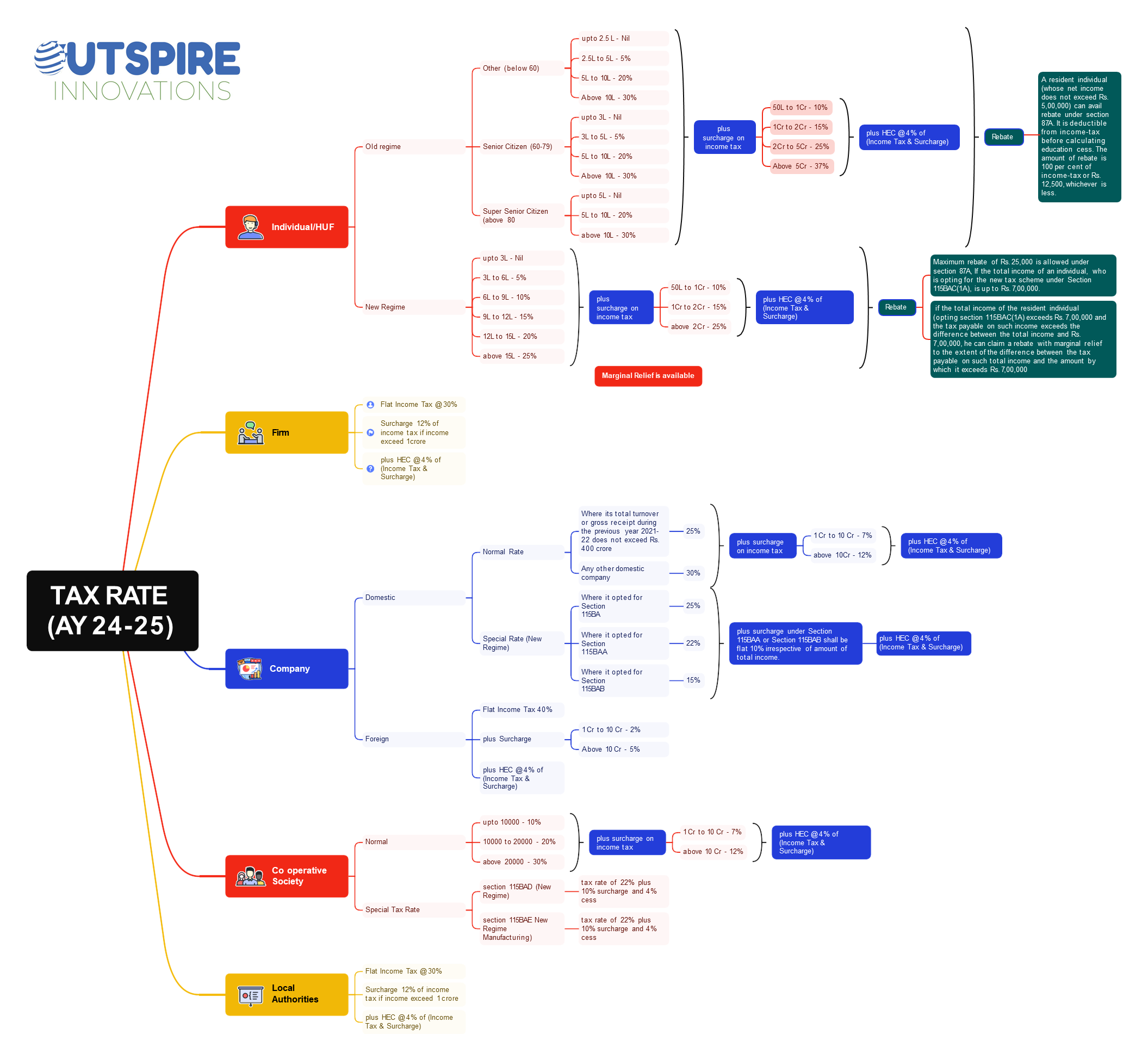

Under the new tax regime, the income tax slabs for FY 2023-24 remain unchanged, ensuring stability and predictability for taxpayers. These slabs are structured to accommodate different income levels, thereby maintaining a fair and progressive tax system.

The income tax slabs under the new tax regime are as follows:

From 0 to 3,00,000: Tax rate of 0%

From 3,00,001 to 6,00,000: Tax rate of 5%

From 6,00,001 to 9,00,000: Tax rate of 10%

From 9,00,001 to 12,00,000: Tax rate of 15%

From 12,00,001 to 15,00,000: Tax rate of 20%

Above 15,00,001: Tax rate of 30%

These slabs ensure a graduated tax structure, wherein individuals with higher incomes are taxed at higher rates, thereby maintaining progressivity in the tax system.

Changes Announced in Budget 2023

Budget 2023 introduced several changes to the new tax regime, aimed at making it more attractive for individual taxpayers. These changes include:

- Default Option: Making the new income tax regime the default option, unless individuals opt for the old regime explicitly.

- Increased Rebate: Increasing the rebate under Section 87A to taxable income of Rs 7 lakh, providing tax relief for individuals with lower incomes.

- Raised Exemption Limit: Raising the basic exemption limit to Rs 3 lakh from Rs 2.5 lakh, reducing the tax burden on taxpayers.

- Simplified Tax Structure: Reducing the number of income tax slabs from six to five, simplifying the tax structure.

- Standard Deductions: Introducing a standard deduction of Rs 50,000 for salaried individuals and pensioners, providing additional tax relief.

- Benefits for Family Pensioners: Allowing family pensioners to claim a standard deduction of Rs 15,000, further enhancing tax benefits.

- Reduced Surcharge: Lowering the highest surcharge rate from 37% to 25%, reducing the overall tax burden on high-income earners.

These changes aim to streamline the tax system, reduce compliance burden, and provide relief to individual taxpayers across different income levels.

Income Tax Slab Rates for FY 2023-24 under Old Tax Regime

For individuals opting for the old tax regime, the income tax slabs remain unchanged from the previous financial year. These slabs vary based on the age and status of the individual, providing different exemption limits and tax rates.

The summary of income tax slabs under the old tax regime is as follows:

- For individuals below 60 years of age: Basic exemption limit of Rs 2.5 lakh

- For senior citizens (aged 60 years and above but below 80 years): Basic exemption limit of Rs 3 lakh

- For super senior citizens (aged 80 years and above): Basic exemption limit of Rs 5 lakh

- For non-resident individuals: Basic exemption limit of Rs 2.5 lakh

These slabs cater to different segments of taxpayers, offering specific exemptions and rates based on their age and residency status.

How to Calculate Income Tax Payable Under New Tax Regime

Calculating income tax under the new tax regime involves several steps:

- Determine Gross Total Income: Including salary, pension, and other sources.

- Subtract Standard Deduction: Rs 50,000 and deductions under Section 80CCD(2) for NPS contribution.

- Arrive at Net Taxable Income: The amount on which tax is payable.

- Apply Applicable Slabs and Rates: Calculate tax payable.

- Compute Cess: At 4% on the total tax payable amount to arrive at the final tax liability.

- An illustrative example of calculating income tax payable under the new tax regime can help taxpayers understand their tax obligations effectively.

Calculation of Income Tax Liability Under Old Tax Regime

Similarly, taxpayers opting for the old tax regime can calculate their income tax liability using applicable slabs and rates. Deductions and exemptions under various sections of the Income Tax Act can further reduce the tax burden.

Following a similar process of determining taxable income and applying relevant slabs and rates enables taxpayers to arrive at their income tax liability under the old tax regime.

Determining Income Tax Slabs

The choice between the old and new tax regimes depends on various factors, including income levels, available deductions, and individual preferences. Taxpayers should carefully evaluate both options to choose the regime that offers maximum benefits and aligns with their financial goals.

Comparing income tax slabs, rates, and available deductions under both regimes facilitates decision-making and ensures optimal tax planning.

Surcharge on Income Tax

Surcharge is an additional tax levied on individuals with higher incomes. The rate of surcharge varies based on the income level and status of the taxpayer. Understanding the surcharge provisions is essential for accurate tax planning and compliance.

Marginal Relief

Marginal relief provides relief to taxpayers in situations where the actual tax payable exceeds the regular tax liability due to surcharge. By ensuring fairness and equity in taxation, marginal relief minimizes the tax burden on taxpayers.

Income Tax Slabs for Previous Financial Years

Reviewing income tax slabs for previous financial years helps taxpayers track changes in tax rates and plan their finances accordingly. Historical data on income tax slabs provides insights into evolving tax policies and their impact on individual taxpayers.

Conclusion

Understanding income tax slabs for FY 2023-24 (AY 2024-25) is essential for effective tax planning and compliance. By familiarizing themselves with applicable slabs, rates, and deductions, taxpayers can optimize their tax liabilities and achieve financial goals.

Explore additional resources and tools to enhance your understanding of income tax slabs and optimize your tax planning strategies. Take advantage of professional tax advisory services to navigate complex tax regulations and maximize tax benefits.